Since the beginning of time, the world and its citizens have experienced and witnessed the before, during, and after effects of extreme levels of optimism, euphoria, fear, and greed. In this series of articles, we explore the history of financial bubbles, why they happen, and most importantly, how you can avoid becoming the victim of their often devastating impact.

We Are The Summa Group

As advisors to a diverse group of clients over the past 30 years, we have seen how these bubbles impact the psyche of the common investor over time. There are always signs to indicate a shift in investment behavior, decision making, and rationale. In winter 2000, many conversations took place that clearly indicated a false sense of security, complacency, and elevated levels of greed. Clients who had been bond holders their entire lives were now prepared to invest everything in tech stocks. Everyone was suddenly an investment advisor who could easily beat the market returns. The NASDAQ ultimately lost about 85% of its value in a short period of time. Many investors were left in this wake of destruction and are still waiting for a “buy signal.” In fall 2007 as I sat in the chair to get a haircut, the stylist was sharing that she had just purchased her third home. Perhaps she was the best paid in her profession, but this was a bit unusual. She continued to share how little proof of income, assets, and other signs of financial stability were required to get approval for these very high debt-to-value loans. Shortly after this conversation, the 2008 financial crisis ensued and many were left with little to show for their real estate activities.

We are not in the business of making predictions or bets with our clients’ capital even when our conviction levels are highest. Our job is to protect our clients from what can go wrong in a world that is sometimes complicated. We are living in a global economy where news and information, real and make believe, travel at light speed. A conversation at a coffee shop in Copenhagen overheard by a stranger suddenly becomes fact at a Starbucks in Beverly Hills. This is the world we are living in and it has made our jobs all the more challenging. Social media has permeated the investment landscape in a profound way. Some positives have been derived from this new age, but the dangers of misinformation are cause for alarm.

Photo by PiggyBank on Unsplash.

Series Intent

The intent of this series of articles is to educate while providing a historical perspective on past bubbles and how we as advisors and investors can better navigate the next potential bubble. We suggest that there are a few areas where signs of greed and euphoria are taking shape and we will share some views on this.

On the real estate front, price appreciation has been occurring for many years without a significant correction. Is this because of the massive amount of liquidity in the pockets of buyers, historically low mortgage rates, or simply demographic reasons? In the world of crypto, there seems to be an almost insatiable appetite for all things tied to this relatively new form of currency. It’s definitely notable that Crypto.com paid $700 million for the new naming rights to the former Staples Center, home of the Los Angeles Lakers. We are not in a position to predict the future of residential real estate or crypto assets, but we are in the business of making sure our clients don’t put themselves in harm’s way. Time will tell how all of this plays out. Above all, we care about the stability and growth of our clients’ balance sheets and financial well-being.

Summa and other elite wealth management teams choose to have a repeatable research and due diligence process to help us make investment decisions. As we discuss in these articles, these battle-tested processes go a long way toward insulating us from making decisions fed by fear and greed. They help us provide our clients with a plan that’s based on life goals, directly tied to living a life that satisfies their most cherished objectives.

History and Main Causes of Financial Bubbles

Financial (or asset) bubbles are marked by sharp price appreciation in asset prices over a period of time, sometimes lasting years, followed by an inevitable crash. Before examining how and why bubbles form, let’s review a few notable ones throughout history.

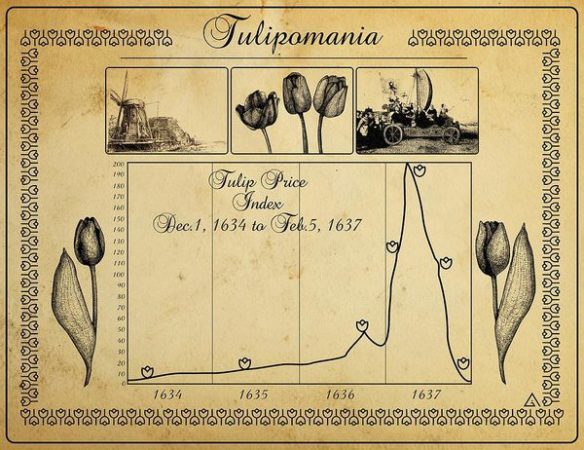

Tulip Mania (1634–1637)

Tulip Mania was one of the earliest recorded asset bubbles. In the 16th century, Western Europeans brought the tulip plant from the Ottoman Empire to Europe, where its rarity and exotic beauty eventually became a status symbol and attracted speculators from a wide cross-section of Dutch society in the 1630s. The price of a tulip bulb reportedly increased twentyfold between November 1636 and February 1637 (prices surged to the equivalent of tens and hundreds of thousands of dollars in today’s money), only to plunge 99% in three months. Many people lost fortunes and the Dutch economy sank into a mild depression.

Source: Amsterdam Tulip Museum

Wall Street Crash (1929)

A few years after the end of World War I, the American economy underwent a boom, and the stock market soared amid commercialization of new technologies, such as the airplane, automobile, and radio. The era became known as the Roaring ’20s. Among other things, borrowed money (aka margin) and herdlike behavior fueled stock market speculation. Even though the “official” crash occurred on October 29, 1929 (aka Black Tuesday), prices continued to drop and finally bottomed out three years later. The repercussions were widespread and devastating, with suicides, sky-high unemployment, millions thrown into poverty, and thousands of bank failures during the Great Depression that followed.

Japanese Economic Bubble (1980s)

In response to a mid-1980s recession, the Japanese government undertook an aggressive fiscal and monetary stimulus to turn the nation’s economy around. The plan worked too well—the subsequent economic boom resulted in Japanese stock prices and urban land values tripling between 1985 and the bubble’s peak in 1989. Japan’s economy deteriorated after that, as stocks and real estate slid and led the country into an agonizing period of deflation and stagflation (high inflation rate with slowing economic growth rate), known as the lost decades and lasting more than 20 years.

Internet/Dot-com Bubble (late 1990s)

The internet bubble (aka the dotcom or tech bubble) was a classic case of mass-market hysteria. The excitement of the emerging internet lured investors into the stocks of internet-related names like Webvan.com, Pets.com, eToys.com, and many others that were burning through piles of money and had not yet even turned a profit. Valuations went through the roof, but many believed that earnings did not matter. The tech-dominated NASDAQ Composite Index spiked to a new high (above 5,000) in March 2000, then dropped like a rock (losing nearly 80% from the peak) before bottoming out in October 2002. Not surprisingly, a recession followed shortly after the peak.

U.S. Housing Bubble (2007–2009)

The housing bubble was a painful reminder that investors have short memories. Even as the economy and financial markets emerged from the wreckage of the internet bubble, a new home-buying mania took shape. Mortgage loans were offered to pretty much anyone regardless of their income level or credit score. In retrospect, plenty of warning signs were there: unsustainable consumer debt, rampant mortgage fraud, mounting defaults, willful ignorance of credit deterioration in mortgage-related securities—yet, most investors looked the other way. The resulting global financial crisis was the worst economic contraction since the Great Depression, and the world continues to feel some of its effects to this day.

How Do Financial Bubbles Form?

According to Chris Butsch of Money Under 30, financial bubbles have five stages:

- Displacement: Also known as the excitement stage, this is when a small first wave of investors notices the opportunity and invests.

- Boom: The greater population learns about the opportunity and a second, larger wave of investors starts to pour money in.

- Euphoria: Investors from the excitement and boom stages start getting rich, at which point everyone else starts to notice and invest.

- Profit-taking: Experienced and institutional investors start to pull out. This causes prices to begin slowing down and leveling off, which signals other experienced investors to begin heading for the exit too.

- Panic: Everyone tries to pull out, generally all at the same time, pushing prices down much lower.

Why Do Financial Bubbles Form?

While each bubble may have its unique catalyst, we believe that there are several common psychological aspects that play significant roles in creating financial bubbles. The field of behavioral finance suggests that investors have a number of biases that can influence how they make financial decisions, often in irrational ways. We will examine three of them.

Photo by Lightspring on Shutterstock.

1. Overconfidence Bias

Most people tend to overestimate their skills, whether it’s driving or picking stocks. In investing, overconfidence bias often leads people to overestimate their understanding of financial markets or specific investments and disregard data and expert advice. This often results in misguided attempts to time the market or build concentrations in risky investments they consider a sure thing. In addition, this overestimation of risk tolerance leads to investment strategies that don’t truly align with their needs. In general, overconfidence bias tends to trick the brain into believing it’s possible to consistently beat the market by making risky bets, often ignoring market fundamentals, which can be a recipe for disaster.

2. Herd Mentality

Humans are naturally prone to herding. People join any number of herd groups—social, religious, political, sports, and others. They rely on the mutual support found in these settings and the information sharing that occurs in the group. Investing is no different when it comes to herd mentality. However, it is often uninformed investors, and those with the most to lose, who form the bulk of the investing herd. Trying to get rich quickly by following the example of successful traders, they wind up losing everything. Herd mentality all too frequently results in the herd “running off a cliff” together. The history of markets is replete with examples of investors driving markets drastically upward, only for herd panic to crash those markets.

3. FOMO (Fear of Missing Out)

FOMO is the fear that someone else is doing something better or more interesting than you are. It’s a common human feeling that’s become much more prevalent recently with social media. When colleagues or friends boast of windfall profits on the stock market, it can cause you to feel envious and dissatisfied with your returns, and question your own investment strategy. FOMO can cause individuals to make irrational decisions that harm their overall investment plans. What doesn’t help is the recent introduction of ETFs that are designed specifically to play to the trend-chasing crowd, with such tickers as BUZZ (VanEck Social Sentiment ETF) and FOMO (Fear of Missing Out ETF). Investing solely based on FOMO usually doesn’t end well, if history is any guide.

What about today? Are there areas within the financial markets that exhibit signs of euphoria? We’ll examine this in Part 2: Current Financial Trends.

Brian Werdesheim is a Managing Director of Investments with The Summa Group of Oppenheimer & Co. Inc., a wealth management company ranked as one of the top financial advisors in the United States.