Josh Schuster was on top of the world just a few short years ago, developing nine-figure skyscrapers in Manhattan. An unforeseen pandemic (and if we’re honest, some overconfidence) may have knocked him off his lofty perch atop New York City real estate, but he’s looking to get back to those heights. This time, instead of developing buildings from the ground up, he’s thinking top down: solar panels.

Like many New Yorkers, Schuster came to Florida during the pandemic, seeking a fresh start and new business opportunities. But not many of them had done more than $1 billion in development deals before the age of 40, with more in the pipeline—before COVID spooked the luxury development market and forced Schuster to find his next move.

Growing up in Ohio, the grandson of a real estate executive, Schuster was always a motivated person, precocious beyond his years. After graduating from college in Louisiana, he worked for a real estate developer in New York, ostensibly to learn the ropes. But Schuster had bigger plans.

About a year and a half into the job, several members of the senior team departed, giving him the opportunity to step up and take on more responsibility.

“I had a go-getter approach,” Schuster says. “I took a lot of notes, I did a lot of research because I wanted to make sure that when I went into a room full of professionals I understood what I was talking about. That was the real reason I was able to garner respect and lead with authority.”

Before long, Schuster was leading a $250 million project—substantial for someone right out of school. After successfully executing on that deal, his boss put him on other large projects, working in markets including New York, South Florida, California, and Las Vegas, where he continued to prove himself as a leader.

About five years into his career, Schuster was seeking a bigger opportunity and decided to take some more risk and raise capital on his own.

“I said, ‘If there’s any good time to take a risk now would be it, right? I’m not yet married, I don’t yet have kids.’ And I went to a family friend with an investment opportunity,” Schuster says.

He raised $30,000, which he used to buy a controlling interest in a property on the Lower East Side of Manhattan that was a seven-story renovation. He convinced two high-net-worth brothers to invest, with a structure that gave Schuster a disproportionate share of profits if he was able to deliver a certain return on capital.

With a creative business plan that targeted modeling agencies and students, the project exceeded its targets and delivered Schuster a sizable windfall. He rolled those profits into other, successively larger deals.

Schuster working in his office

BUILDING AN EMPIRE

After a string of uninterrupted early successes, Schuster continued raising capital, building an increasingly vast network of funding. He sought out high-net-worth individuals and family offices, which he described as “nimble capital” that was willing to bet on a young entrepreneur with a solid business plan and winning track record.

“They invested in the business plan, the real estate, and me,” Schuster says. “But it’s the economics of the deal that really pushes someone over the edge to say yes.”

Those economics were working well, making successive fundraising easier. Soon, Schuster had built a network of more than 140 family offices and high-net-worth groups, and raising capital for deals was almost just “passing the hat,” as Schuster describes it.

That system worked well for years, but as the projects Schuster had access to became larger, doing this a la carte, one-off fundraising became a heavy lift. Big-time real estate developers raise dedicated funds, and that was the sensible route for Schuster at this point.

He started negotiating with a group based on the West Coast, but as they neared the finish line, a once-in-a-lifetime opportunity emerged: A blue chip New York investment firm, Silverpeak—which has acquired more than $25 billion in gross asset value—wanted to invest in Schuster. Not only that, Silverpeak was willing to incubate Schuster’s nascent firm, and provided office space in its Midtown Manhattan building, a few floors up from Nobu.

So in 2016, Schuster jumped on that opportunity and formed Silverback Development, a luxury development firm that took on ambitious, signature projects. With plentiful investment capital and a tailwind of momentum created by his previous success, Schuster eventually grew his “one-man band” into a “symphony” of 18 professionals, developing real estate across five different states. However, going so fast opened the firm up to a harder crash when things turned.

“Like most developers, we were leveraged,” Schuster says. “I was signing personal guarantees with banks and investors. Starting in this business young and never getting a formal education on what these documents mean, and all of a sudden you’re staring down the barrel of a personal guarantee in the nine-figure range. That’s pretty scary.”

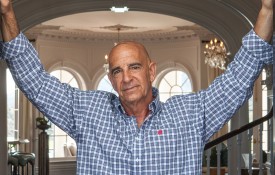

Schuster is the Co-Founder of Solarback LLC, a solar energy company that transforms roofs into a valuable source of long-term passive revenue for property owners and management companies.

Schuster had overachieved at a young age and had never gone wrong betting on himself. He kept doubling down and eventually found himself without the winning hand.

“I was overly confident,” he says.

Also, as he grew his fundraising base and brought on more risk-averse investors, such as family offices, winning them and their substantial purses over with a polished sales pitch and track record of success, he had to make accommodations for partners that were not always perfectly ideologically aligned. That ended up playing a role in Silverback’s demise.

To bring these family offices into the fold, Silverback offered an investment vehicle Schuster called “dequity”—essentially short-term convertible debt. Investors could start out by providing this debt, which would have an option to convert to equity on pre-scheduled terms, usually within six to 12 months. Schuster says these family offices and high-net-worth groups would almost always like what they saw, and 90% would convert to equity, moving from creditors to investors. That was prior to 2020.

“The problem is, when COVID hit and it became time to convert that debt into equity, what rational person was going to do that in a ground-up condo in New York City during a pandemic, when everyone’s fleeing, when hundreds of thousands of people are dying, and the supply chain is completely cut off?” Schuster says. “Nobody. That’s kind of what happened to me.”

With all the family offices still creditors and seeking repayment, Schuster was hit with insurmountable debt obligations he couldn’t satisfy the way he was used to: by raising new capital. He defaulted on this debt and judgments were issued, forcing him to essentially start over.

“I think it was a valuable lesson in what not to do as an entrepreneur,” he says.

Schuster decided to refocus his energy toward a new opportunity, at the crossroads of real estate development and renewable energy

THE NEXT CHAPTER

After being “punched in the gut,” and losing a lot of his longtime financial backers, Schuster had to start thinking about his next move.

“There are a lot of best friends I’ve lost,” he says. “There are a lot of business relationships that were super close that I’ve thrown away, and I have to look at myself in the mirror, and it’s hard to shut the door on the past.”

He decided to refocus his energy toward a new opportunity, at the crossroads of real estate development and renewable energy.

“I was able to sort of reset and figure out what the next chapter of my life is going to look like,” Schuster says. “How will I do it differently? How will I improve on the things that I’ve already accomplished? How do I take the skills and sort of hone them a little bit better for this next cycle?”

That’s easier when you have market-tested real estate skills at the highest level, like Schuster, and a deep understanding of the needs of property owners. It turned out that all he had to do to find his way forward was to look up—at the sun.

That led to Schuster co-founding Solarback, a company that uses a proprietary solar array to generate long-term passive income for property owners and managers by taking advantage of underused rooftop space. South Florida has a lot of rooftops that may not be cool enough for swimming pools and nightclubs, but are hot (and sunny) enough for solar panels. Schuster’s goal is to provide not just significant revenue to property owners, but an amenity that appeals to tenants and generates clean energy for the community, a true win-win-win.

And while Schuster can’t change history, he’s now at peace with it and completely focused on what’s ahead.

“It has taken me a good year, at least, to come to the conclusion that I have to stop hoping for a better past,” he says. “The past is done. I can’t change it. And now I just need to take those lessons, look forward, and hopefully be better all around.”

After some time in the dark, the sun is shining on Solarback—and Josh Schuster—again. In business, the second act is often the most meaningful. In more ways than one, Schuster is seeing the light.