The pace of innovation in the technology sector continues to accelerate while having a massive impact at the company, industry, and global levels. Twice during the past several years, I have shared my views on what many refer to as the Fourth Industrial Revolution. My first featured article on the subject, “The Industrial Revolution of the 21st Century” (November 2019), discussed the embedded themes of artificial intelligence (AI), machine learning, and big data, and how every industry is being disrupted by these irreversible trends. My second article, “Innovation, Disruption and Opportunity” (March 2021), provided a historical perspective on past industrial revolutions and why the current one is different.

Fast-forward to the summer of 2022 and a lot has changed regarding valuations, the appetite of private equity for investing in innovation, and what the road ahead may look like. As with any period of rapid innovation, opportunity, and capital formation, the journey takes many turns and is never without challenges. As of the writing of this article, there are a number of factors impacting the pace of investment, valuations, and the futures of public and private companies. I will share our views on the challenges, dislocations, and opportunities that have materialized as a result of this pendulum swing. Having been an observer of capital markets for more than three decades, my perspective is based on personal experience of investing billions of dollars of capital during many dynamic and challenging market cycles.

Our team is dedicated to differentiating between what is real and what is imaginary. Our conviction levels with regard to the opportunities materializing as a result of this unprecedented era of innovation are unwavering during this period of pause. We will look back at the late ’90s and early 2000s for comparisons and contrasts to the current period. While history rarely repeats itself precisely, it often rhymes. Many of the most prolific companies today were left for dead after the dot-com bubble of 2000. We do not think this period will be much different; when we look back at current valuations, we will find truly magnificent companies were trading at dirt-cheap prices. With a rapid pace of innovation comes rapid obsolescence and therefore there will be plenty of “roadkill” along the way. With an eye on the past and a focus on the future, we are providing discipline and guidance on how investors should be capitalizing on one of the greatest periods of innovation in history.

THE CHALLENGES

In 2002, the technology industry emerged from the dot-com crash in complete decimation, with a bleak outlook on its future. However, two decades later, technology and innovation are at the center of almost every industry. We believe this transformative wave of technological innovation, often referred to as the Fourth Industrial Revolution, will fundamentally change the way we live, work, and interact, and will disrupt businesses globally. That said, the innovation space and the broad tech industry have not been immune to short-term challenges.

The tech-heavy S&P 500 experienced an exponential recovery during the pandemic, doubling from its March 2020 bottom in under a year. The perfect storm of low interest rates and massive bond purchases by the Fed created an environment that was simply unsustainable. Valuations got ahead of fundamentals while investors succumbed to a FOMO (fear of missing out) mentality.

As markets began to realize that the pull forward in technology demand from COVID was not permanent, growth stocks also braced for another headwind: the end of easy money. In mid-2021, the Fed still viewed inflation—which resulted from unprecedented levels of fiscal stimulus, monetary easing, and supply chain disruptions throughout 2020 and 2021—as transitory. As this narrative proved not to be the case and inflation persisted, the Fed changed its tune in November 2021, planning on hiking rates, fast. The 10-year U.S. Treasury yield nearly doubled in a matter of four months to begin 2022. This put valuations front and center—and the very same tech/growth darlings that skyrocketed in the COVID boom fell into a sharp sell-off in January 2022. As inflation persisted and rates climbed higher, the first half of 2022 was marked by a turbulent decline of the tech/growth space, one that can only be likened to a reversal of the pandemic-induced tech boom that occurred just two years earlier.

So, what do rising interest rates have to do with innovative companies? A vast majority of the companies in the innovation space tend to be high-growth companies that are priced based on future earnings. These companies are heavily reliant on capital for future business expansions, and thus utilize debt markets in order to finance their growth. Valuations then must reflect the change in borrowing costs thus negatively affecting stock prices. Investors that once shrugged off excessive valuations due to low interest rates now seek undervalued, cash-flowing businesses. “What can you do for me in 10 years?” quickly becomes “What can you do for me now?”

The destruction of valuations in the public markets in the first half of 2022 did not come without consequences. These start-up tech companies that benefited from heavy investment and massive initial public offerings (IPOs) during the pandemic are now struggling with growth and profitability in the face of a tight money supply and high inflation, with global uncertainty looming. Companies that received multibillion-dollar IPO valuations in 2021 were laying off employees by the hundreds and struggling with profitability not even a year later. IPOs have grinded to a halt in 2022. Private investment in innovation, once accompanied by the “blank check” mindset, has done a complete 180, and start-ups are now struggling to raise capital. Let’s be clear, this outcome was highly predictable and is consistent with past periods where optimism dominates and risk controls become lax.

As seen over the course of history, challenges are inevitable. These challenges, however, ultimately present opportunities for investors to capitalize when valuations are depressed and fear is at its highest level. This time is no different. To be successful in this endeavor, we must observe the challenges, identify the ensuing dislocations, and take action on the opportunities. We will discuss current dislocations at play in the next section.

THE DISLOCATION

As market dynamics changed at the beginning of 2022, many investors were caught offside. This in turn caused panic selling in the tech/growth space. Higher multiple stocks were dumped in exchange for less expensive positions. This was not because the higher-growth businesses no longer provided intriguing long-term benefits, but rather that they simply posed more risk in the immediate term. This near-term mindset has created an environment where innovative companies—and tech/growth in general—are being disproportionately penalized.

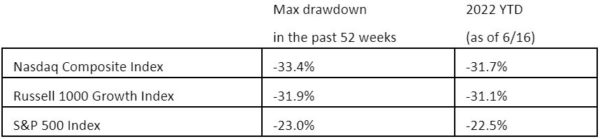

In the first half of the year—or up until June 16, 2022, specifically, which was the date of the recent low—the Nasdaq Composite Index and Russell 1000 Growth Index, both of which are technology dominant, sold off much more significantly versus the broader equity market (S&P 500).

After three consecutive years of strong returns in the stock market (particularly in the growth area), moderate pullbacks were expected, but the severe sell-off we witnessed in the first half of this year is indicative of an underlying dislocation: Valuations are not reflecting strong company fundamentals.

With respect to high-growth companies, many stocks have been punished severely for a lack of earnings visibility and/or not beating earnings expectations. For multiple decades, many growth-oriented companies within the innovation space have been engaging in the “land and expand” strategy, which basically means starting small with your customers, gaining their trust, then expanding into other areas of their business. To say it another way, land as many customers as you can early and expand the relationships (“first-mover advantage”). To accomplish that, most growth companies put a significant portion of their revenues into business reinvestment in order to sustain growth (mainly via sales, marketing, and R&D efforts), but reinvestment dampens earnings from surface level, which effectively depresses the company’s valuation. Historically, fast-growing companies will reinvest most, if not all, of their free cash flow back into the business in order to grab market share and expand into other strategic business opportunities. In the short term, this can negatively impact how they look on paper. Today, the market is not differentiating between companies truly dedicated to a long-term runway and companies solely focused on meeting quarterly numbers.

Let us examine the dislocation between current valuations and company fundamentals from a psychological perspective. In one of his memos, Howard Marks of Oaktree Capital talked about “pendulum,” not as a mechanical model (which is predictable in terms of time and pace) but more as “mood swings.” Applying this concept to investor psychology, investors can certainly become euphoric at times and downright miserable at others. That said, these swings to either extreme are not the norm—the majority of the time, the pendulum remains in a realistic middle territory. This middle ground is where investment decisions are made based on fundamentals rather than emotion. We saw market euphoria throughout 2021, and now we seem to be near or at the other end—the miserable end—of the pendulum.

In this type of difficult environment, the average investor tends to panic and exit the market (the “get me out of here” mentality), usually at the wrong time. We’re seeing this phenomenon play out across many types of assets—stocks, bonds, bitcoin, etc. Investors have been selling indiscriminately, or “throwing the baby out with the bathwater.” Particularly with respect to growth stocks, investors have not been distinguishing between high-quality growth stocks (those with healthy profit margins, low debt, steadily growing revenues, etc.) and low-quality growth stocks (those with low/no profit margins, high debt, etc.) during this year’s sell-off. If history is any indication, post-capitulation is where we will again see a focus on fundamentals and a market that rewards truly great companies. One important thing to keep in mind is that, as Howard Marks has said, while timing is uncertain, investor sentiment will eventually settle in a more stable place for an extended period of time.

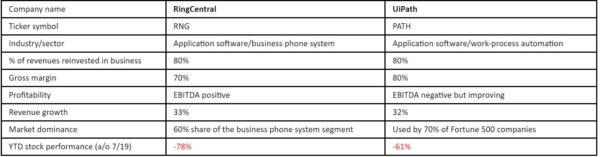

As stated earlier, we are seeing a dislocation between the current valuation/price and company fundamentals, particularly among certain high-growth companies. For example, let us examine RingCentral and UiPath, two of the fastest-growing companies with a dominant market share. By every measure, these companies’ fundamentals look strong, yet their stocks have been punished severely this year—a clear dislocation!

This is not the time to run for the hills. In fact, the current dislocation in the stock market is presenting investors with tremendous opportunities, particularly in the growth/innovation space, if you have a mid- to long-term investment horizon. This is what we will examine in part two.

Brian Werdesheim is Managing Director of Investments with The Summa Group of Oppenheimer & Co. Inc., a wealth management company ranked as one of the top financial advisors in the United States.

SOURCES

- Gillham, Jonathan. (2017). The Economic Impact of Artificial Intelligence on the Global Economy.

- How Big Tech Won the Pandemic – The New York Times (nytimes.com)

- The Fed’s Liquidity Confusion | AIER

- One Year Into the Pandemic, Big Tech Is Bigger Than Ever – Bloomberg

- After Covid-era boom, newly public tech stocks hit first major hurdles (cnbc.com)

- S&P 500 doubles from its pandemic bottom, marking the fastest bull market rally since WWII (cnbc.com)

- Pandemic-stocks: Covid drove massive market gains — what happens next (cnbc.com)

- Tech Stock Valuations, COVID-19, And The Efficient Market Hypothesis: Enough Already | Seeking Alpha

- Covid has made biotech companies the hot new tech sector as investor demand drives record IPOs (cnbc.com)

- Microsoft CEO: “We have seen two years’ worth of digital transformation in two months” – DCD (datacenterdynamics.com)

- Howard Marks Memo to Oakree Clients: Conversation at Panmure House

- Number of Years It Took for Different Products to Gain 50 Million Users (earthlymission.com)

- Bessemer Venture Partners. (2020). State of the Cloud 2020. https://www.bvp.com/atlas/state-of-the-cloud-2020

- Credit Suisse. December 2019. U.S. Equity Strategy Navigator. https://research-doc.credit-suisse.com/docView?language=ENG&format=PDF&sourceid=em&document_id=1081975521&serialid=4d5G6pkBcRgbhbjfabXIVlkbBEv40ngzw0LDTOzVpX0%3d

- Gartner Says More Than Half of Enterprise IT Spending in Key Market Segments Will Shift to the Cloud by 2025