In November 2019, I first shared my views on the current innovation cycle. Sixteen months later, the cycle has accelerated and we continue to be excited about the opportunity to invest in and capitalize upon what we believe is the first large-scale, wide-in-scope cycle of technological innovation since the internet wave of the mid-’90s.

We believe this transformative wave of technological innovation, often referred to as the “Fourth Industrial Revolution,” will fundamentally change the way we live, work, and interact, and will disrupt businesses globally. Moreover, we believe technology companies, because of the coronavirus crisis, are likely to increasingly benefit, permanently and secularly, from strong trends toward distributed workloads, “work from everywhere,” and the cloud and SaaS/app ecosystem that supports this decentralized user architecture, with security, redundancy, and agility in its deployment and ease of infrastructure scaling. This paradigm change in user behavior, we believe, is likely to not only sustain momentum post-pandemic, but also fundamentally change human-to-business interaction in a secular matter, and digitally transform business collaboration, learning, and training, and the entire sales activity cycle.

During our careers, we have seen waves of innovation run through the capital markets, but never like what we see today. Innovation is not only impacting every major industry, but it’s also impacting everyday life for Americans and others around the world. Likewise, innovation is not just something that companies are evaluating and considering—it’s a necessity. If not fully embraced and acted upon with the complete dedication and force of their intellectual and financial resources, they may regret it. Never before have we seen such a wide disparity between how much a company spends on R&D and its growth rate. The correlation between investment and stock performance is staggering across all industries but especially in healthcare and technology. The bottom line is, companies who are investing in R&D are being richly rewarded while those who are not are subjecting their future to untold risk.

THE HISTORY OF INDUSTRIAL REVOLUTIONS

We believe we are living through the beginning stages of the Fourth Industrial Revolution today and that it is driving the current pace of technological innovation in the marketplace. Throughout history, people have always been dependent on technology. Of course, the technology of each era might not have the same dimension as today, but for their respective times, each certainly provided the public with something to marvel at.

People would use the technology they had available to help make their lives easier and at the same time try to perfect the technology and bring it to the next level. This is how the concept of the industrial revolution began. Before examining the current industrial revolution, let us first try to understand the three previous industrial revolutions.

Source: Franklin Templeton

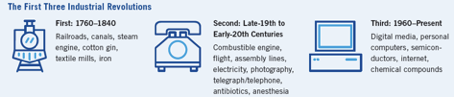

The First Industrial Revolution (1760–1840)

The First Industrial Revolution marked a period of development in the latter half of the 18th century that transformed largely rural, agrarian societies in Europe and America into industrialized and urban centers. Fueled by the seismic change wrought by use of steam power, the First Industrial Revolution began in Britain and spread to the rest of the world, including the United States, by the 1830s and 1840s.

The biggest changes to the country and the economy came in the form of mechanization. This initiated the great shift from an agrarian to an industrial society, over time, and provided a necessary backbone to bolster the power and expansion of the broader economy. At the time, the massive extraction of coal along with the very important invention of the steam engine created a new type of energy that sped up the manufacturing of steel and railroads, which accelerated the economy, and built cities and connected them.

The Second Industrial Revolution (late 19th century to early 20th century)

Almost a century following the First Industrial Revolution, the world experienced a second. It started at the end of the 19th century, with immense technological advancements that helped the emergence of new sources of energy: electricity, gas, and oil.

The results of this revolution included creation of the internal combustion engine. Other important aspects of the Second Industrial Revolution were the ubiquitous demand for steel, the advent of chemical synthesis, and proving the methods and manufacturing of communication such as the telegraph and telephone.

The development and acceptance of the automobile and the airplane in the beginning of the 20th century impacted life and the economy to such a degree that, even today, they not only epitomize that era, but still define how we travel today. Mechanized advances required for war stimulated wide-ranging industrial expansion and application, and helped establish the United States as the power it was to become.

The Third Industrial Revolution (1960–present)

Another century passed and we bore witness to the Third Industrial Revolution. In the second half of the 20th century, we saw the emergence of yet another source of untapped energy—nuclear power.

The Third Industrial Revolution brought forth the rise of electronics, telecommunications, and of course computers. Through the new technologies, the Third Industrial Revolution opened the doors to space exploration, research, and biotechnology.

In the world of industries, two major inventions, programmable logic controllers and robots helped give rise to an era of high-level automation.

Read more of Brian Werdesheim’s thought leadership.

The Fourth Industrial Revolution

This next iteration of the industrial revolution builds on the foundation initiated in the 1960s and acceleration in the 1990s with proliferation of the internet. The Fourth Industrial Revolution is a technological revolution that will fundamentally alter the way we live, work, and relate to one another. It is “one of the most important revolutions ever. Whereas computer scientists used to specify every instruction one line at a time, now algorithms write algorithms, software writes software, computers are learning themselves. It is the era of machine learning, and a historic time when serendipity meets destiny,” as described by Jensen Huang, CEO of Nvidia.

We don’t view this upcoming cycle of innovation as another mini-cycle, but rather as a broad-based cycle of innovation driven by a unique set of new technologies, including next-gen broadband mobility (5G and Internet of Things), and significant advances on the consumer side in display technologies (3D, VR, and AR) and AI and autonomous driving.

WE’RE STILL IN THE EARLY STAGES

We are still riding the early wave of technological innovation. For example, even 5G, a critical infrastructure layer underneath the compute and application layers, will take years to deploy fully. Big data is as foundational today as the internet was in the 1990s and mobile phones were in the mid-2000s. Only in the last few years have machines begun to recognize images and words better than people. This is a technological innovation decades in the making, which in our view is now enabling an accelerated pace of growth and adoption of AI at a time when major milestones in image recognition, natural character recognition, natural-language processing, and speech recognition are being reached. For example, Alphabet introduced Google Lens that uses AI to let cameras understand what they see.

In summary, recent application advances in AI that were only reached in the last few years are now providing us with confidence that AI is rapidly approaching the cognitive era.

As a result, business leaders are rapidly abandoning legacy models, as multi-trillion dollar industries are now turning to AI to accelerate their digital transformation and enhance their chances of survival.

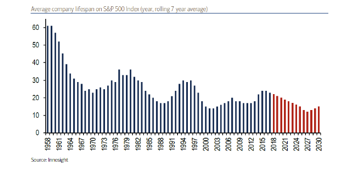

Merrill Lynch has predicted that 50% of S&P 500 companies could be replaced over the next 10 years, as the average tenure of an S&P 500 company is forecast to contract from its high of nearly 40 years in 1977 to 12 years by 2027.

WHAT INVESTORS SHOULD BE THINKING ABOUT REGARDING INNOVATION

Innovation can be looked at through a number of different lenses, but the common theme and basic message is simple: Where there is innovation, there is change and opportunity. Many in society are inherently resistant to change and do not easily embrace the change that comes along with innovation. From an investor standpoint, these individuals will be less likely to embrace the opportunities that will materialize. From a business-owner standpoint, you are likely to be left with a business that can no longer compete with others who have spent the time, resources, and capital to stay in front of the innovation curve.

As an investment advisor, not staying current with how innovation is impacting industry and companies means you’re not giving your clients an opportunity to consider the benefits of a once-in-a-generation experience. As wealth advisors, we are required to think about innovation from many perspectives given the role we play in our clients’ lives. Technology has had a big impact on the way we manage our practice every day. From client service, research, and due diligence to reporting and communication, technology is creating massive levels of efficiency in our ability to collaborate, communicate, and execute on a daily basis and in real time. There are still many advisors who have not invested in their own practices and the many technologies that are enhancing our ability to positively impact the client experience.

The investor must pay attention to all of the ways in which their lives are being impacted by the latest revolution and figure out how to not only benefit financially, but benefit by improving the quality of their lives. With innovation comes the inevitable unintended consequences that can have profound negative implications. Parents with teenagers have to be concerned with how innovation in social media, gaming, and telecommunications is impacting our next generation’s ability to develop into human beings that can engage in more traditional forms of human interaction. Will they have the soft skills and intangible qualities to pursue and obtain jobs that demand high levels of social interaction, problem-solving, and awareness?

We believe the net positives that come from all of this will far outweigh the negatives, but we must be mindful of the challenges ahead. Elite advisors want their clients to embrace innovation, change, and the investment opportunities in front of them.

WHY NOW?

In short, innovation is accelerating and creating investment opportunities now. We are living in a period of unprecedented economic change. This presents us with a compelling backdrop in which to invest. In 1964, the average tenure of companies in the S&P 500 was 33 years. In 2016, the average had shortened down to 24 years, and by 2027, it is expected to be 12 years. The following illustrates how innovation has been accelerating:

Source: Franklin Templeton

THE IMPORTANCE OF PARTNERING WITH THE RIGHT TEAM

Advisors may have the right macro thesis with regard to a specific opportunity, but often have little understanding about how to express and implement their convictions. Therefore, it’s paramount to be aligned with investment professionals who not only have a vision, but have the experience, relationships, and process to act on behalf of the client.

The world is saturated with many opportunities that are sometimes difficult to evaluate. We live in a nuanced world where things are not always what they appear to be. Without going into a dissertation about the pitfalls of this, suffice it to say that it takes decades of experience to properly evaluate an opportunity and access it.

As we observe the opportunity in front of us, we are looking within both the public and private markets. On the public side, an abundance of information is available to anyone willing to invest the time into the research process. The difficult part is picking winners from losers and having a discipline that leads to making more good decisions than bad ones. We choose to rely on time-tested professionals who have been navigating the technology markets for decades. A seasoned team allows investors to gain access to a broadly diversified portfolio of high-quality growth stocks that meet a particular standard. One such manager believes the generation of outsized free cash flow is a determinant of long-term success. They also believe strong balance sheets, high barriers to entry, and great management teams may win in the long run. As it relates to the current innovation cycle, having a team with a vision for what may happen now and in the future is very important.

On the private side, things can get a little more complicated because there is not as much information available. Furthermore, private companies come in different shapes and sizes and with a broad range of risk and return possibilities. We believe there is a huge advantage investing in later-stage private growth companies that are at or near scale and at or near profitability. UiPath and Databricks are examples of companies that successfully completed two late-stage rounds of financing with substantial valuation increases ($10.2B to $35B, and $6.2B to $25B, respectively). Their business models have for the most part been proven and now it’s a function of execution and having the capital to scale quickly while grabbing market share. Even for companies in this position, the road ahead is always uncertain, with intense competition and rapidly changing technologies.

Not dissimilar to how we approach the public markets, we must be with a team of private equity professionals who have the experience and skill to gain some sort of advantage as they deploy capital in later-stage companies. One cannot dispute that private companies are staying private longer and not in a hurry to jump through the IPO door. As a result, substantial wealth creation is occurring in the private space. Those who have the ability to gain access to these companies will have an opportunity to benefit from this trend. Only highly reputable and seasoned private equity professionals are gaining access to these later rounds of financings, so this becomes a barrier for most well-intentioned investors.

Nobody knows for sure how long this current wave of innovation will last, but we are in the first inning and the converging technologies surrounding big data, deep and machine learning, and AI are creating opportunities for software and other technologies at a pace never seen before. No doubt investment careers will be defined by how they choose to play the Fourth Industrial Revolution. It’s human nature to underestimate the longevity and sustainability of deeply embedded trends in technology, healthcare, and other industries where innovation is running rampant.

Learn more about The Summa Group’s approach to wealth management.

CONCLUSIONS

When history books are written about this current period of innovation and how our lives were impacted in positive and negative ways, historians will have a huge canvas from which to work.

AI is, of course, at the very heart of this rapid pace of fundamental secular change. As a result, business leaders are rapidly abandoning legacy business models, as multi-trillion dollar industries are turning to AI to accelerate their digital transformation and enhance their chances of survival.

Importantly, we are just at the beginning stages of this technological revolution, as we continue to develop the physical, compute, and application layers of this new digital world. For example, even 5G, a critical infrastructure layer underneath the compute and application layers, will take years to deploy fully. In particular, 5G is not a single innovation, but rather a set of advances in spectrum usage.

The investment implications are staggering and secular in nature. Against this backdrop of significant disruption, companies are rushing to invest, not to seize the opportunity, but simply to survive the rapidly changing landscape of the fully connected economy. As a result, AI spending alone is projected to grow at 28% annually, approaching $100B by 2023.

The investment opportunity exists in both the public and private markets, with more and more wealth creation happening in the private sector. This dynamic is presenting well-positioned and experienced investors with access to some of the fastest-growing software companies in the world.

We believe we are at the early stages of potentially the most disruptive innovation cycle in technology ever: an AI-driven revolution that by 2030 has the potential to contribute up to $15.7T to the global economy.

Ultimately, if you believe this revolution will impact every major industry—healthcare, finance, transportation, retail, and others—you need a process by which to identify, evaluate, and ultimately select investment opportunities that are well positioned to capture the opportunity in a responsible and strategic manner.

SOURCES

The 4 Industrial Revolutions (June 2019). Retrieved from ied.eu/project-updates/the-4-industrial-revolutions

Industrial Revolution (September 2019). Retrieved from history.com/topics/industrial-revolution/industrial-revolution

How the Second Industrial Revolution Changed Americans’ Lives (January 2019). Retrieved from history.com/news/second-industrial-revolution-advances

The Third Industrial Revolution—Internet, Energy, and a New Financial System (March 2015). Retrieved from forbes.com/sites/goncalodevasconcelos/2015/03/04/the-third-industrial-revolution-internet-energy-and-a-new-financial-system

6 Reasons You Should Invest in Innovation (2020). Retrieved from entrepreneurshipinabox.com/8479/6-reasons-you-should-invest-in-innovation

Investing in Innovation (August 2020). Retrieved from franklintempleton.com/content-common/market-perspective/en_US/investing-in-innovation-u.pdf and franklintempleton.com/forms-literature/download/FDTF-BR

Why AI and Robotics Will Define New Health: Retrieved from pwc.com/gx/en/industries/healthcare/publications/ai-robotics-new-health/transforming-healthcare.html

Advantage Advisers Xanthus letter, Sept. 30, 2020.

Advantage Advisers Xanthus Monthly Update, Oct. 2020.

Federated Kaufmann Insights: “A New Era for Growth Stocks,” May 5, 2020. federatedinvestors.com/insights/article/a-new-era-for-growth-stocks.do

Artisan Focus Fund Monthly Summary, April 30, 2020. artisanpartners.com/content/dam/documents/monthly-commentary/vr/2020/apr/ARTTX-APDTX-MCommentary-0420-vR.pdf

2Q 2020 Artisan Global Opportunities Fund Presentation Deck, June 30, 2020.

Artisan Global Opportunities Fund Quarterly Commentary, Sept. 30, 2020. artisanpartners.com/content/dam/documents/quarterly-commentary/vr/2020/3q/ARTRX-APDRX-APHRX-QCommentary-3Q20-vR.pdf

Manning & Napier Fund, Inc.—Rainier International Discovery Series Commentary, Sept. 30, 2020.

Alkeon Capital Management LLC—Alkeon Innovation Fund Presentation Deck, Nov. 2020.

Artisan Partners Thematic Team—PM Viewpoints: Data-Driven Thematic Opportunities. March 2020. artisanpartners.com/content/dam/documents/pm-viewpoints/vxus/Viewpoints-Data-Driven-Thematic-Opportunities-vXUS.pdf

BofA Global Research—Communications Infrastructure, Sept. 28, 2020. rsch.baml.com/r?q=1Vb!-OoSh0lCYNeD00HeWw__&e=mahearn%40ipipartners.com&h=ORSDbw

Oppenheimer & Co. Inc. does not provide legal or tax advice, but will work with your other advisors to assure your needs are addressed. The opinions of the author expressed herein are subject to change without notice and do not necessarily reflect those of the Firm. Additional information is available upon request. Investors should review potential investments with their financial advisor for the appropriateness of that investment with their investment objectives, risk tolerances and financial circumstances.

©Oppenheimer & Co. Inc. Transacts Business on all Principal Exchanges and Member SIPC 3462709.1